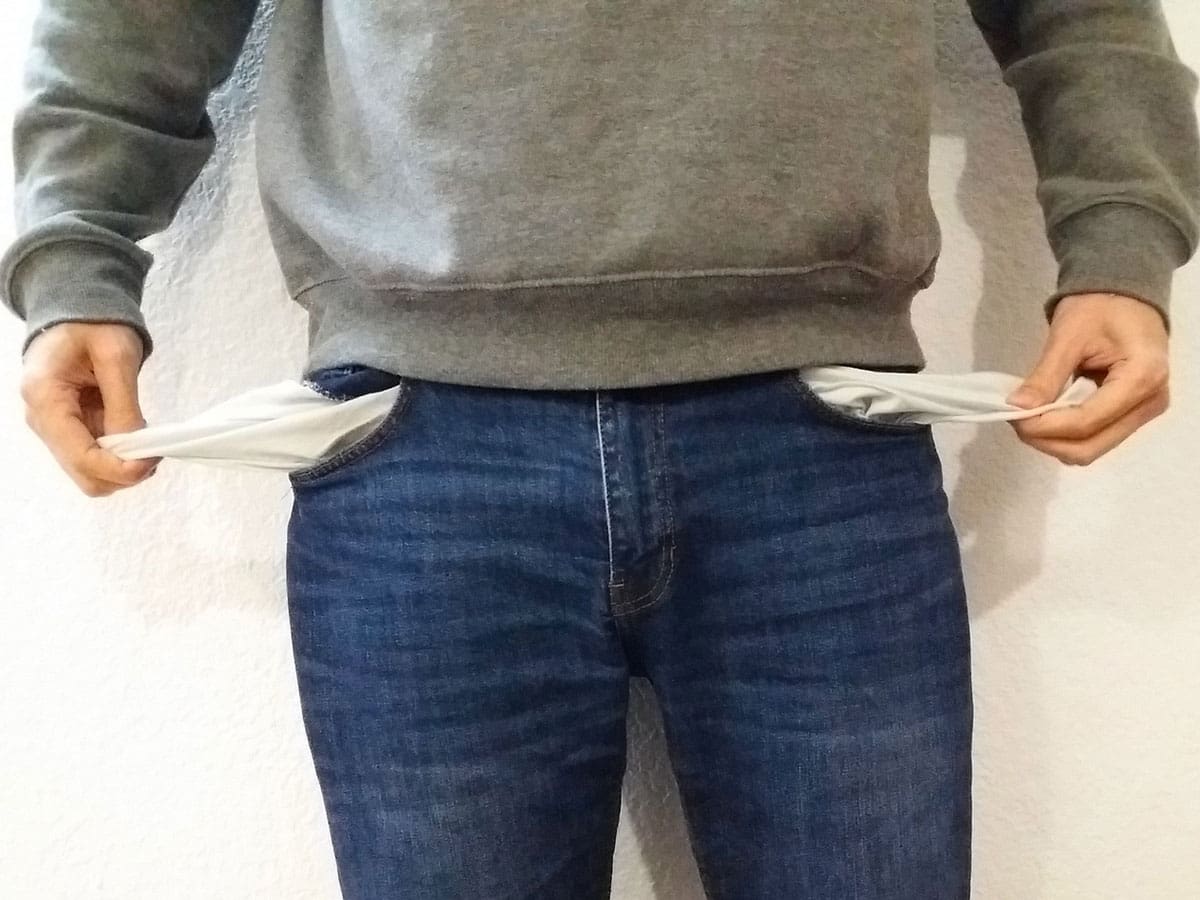

Debt in the UK is now an exponential problem. Without intervention, we risk a spiralling crisis.

80% of UK adults will carry debt into 2021, with 8.9 million individuals and businesses having to borrow more due to the pandemic. So what is the solution?

Chris Leslie, the Chief Executive of the Credit Services Association, has advised the Department for Work and Pensions to encourage early intervention between creditor and debtor to help prioritise early repayment. Leslie argues that effective communication between both parties is the key to controlling the UK’s debt problem.

Use a debt collection agency to deliver the results you need

In his letter, Leslie states early engagement and support is: ‘the best first step to resolving problems.’ If debtors are given the opportunity to discuss their finances with either the creditor or a debt collection agency working on their behalf, Leslie argues they are much more likely to both create and stick to an affordable repayment plan. This pathway provides a solid structure for both parties, and allows debtors to feel more in control of their situation. Constructive communication supports mental health and well-being, and ensures both debtors and creditors are making positive steps to help resolve the issue.

Leslie states that: ‘sharing the issues between all parties is most often the best route to resolution.’

However, if early intervention is ignored, the situation could be unnecessarily prolonged. If creditors are unaware of their debtor’s financial situation or personal circumstances, they are less likely to find a smooth road to resolution. As stress levels increase and additional costs begin to spiral.

Debt collection agencies are changing the narrative

The pandemic has highlighted the crucial role debt collection agencies play in supporting those with debt. And Leslie believes that it was the ‘conversations between customers and lenders’ that made the difference.

In 2020, debt collection agencies in the UK went over and above to support debtors through the pandemic. Three-quarters of a million borrowers received additional forbearance from debt collection agencies. These were supplementary measures offered to those whose finances were negatively affected by coronavirus.

The UK government have already acknowledged the best practice evidenced by the debt collection sector. And Leslie believes more can be done to promote the work of the industry.

Trust Cobra to get your money back

Our specialist team have supported hundreds of debtors who have been affected by the pandemic. Some have seen their finances change overnight; others have been unable to focus on debt repayment due to the loss of a loved one.

We work on behalf of our clients to ensure debtors prioritise repayment, whatever their situation. Where required, we can work with debtors to support them in creating an affordable repayment plan.

We are trusted by clients across the world to get their money back. With clients such as New York Mellon, we offer a truly international debt collection service. So wherever your debtor may be, we will work with them to get you the result you deserve.

Our face-to-face collection method has an industry-high success rate of 89%. And thanks to our clients’ feedback, we hold a 5* Trustpilot rating.

So if you are looking to recover a personal or business debt, trust Cobra to get your money back.

Contact one of the Cobra team on 0151 526 4222. And let’s get started.

Get your money back in your pocket. Where it belongs.